Using VIX to Trade the Market: What Works (and When)

In the ever-evolving world of algorithmic trading, finding robust strategies that can weather different market conditions remains the holy grail for investors. Today, I want to share insights from my analysis of several VIX-based trading strategies that have gained attention in financial circles.

What We’re Examining

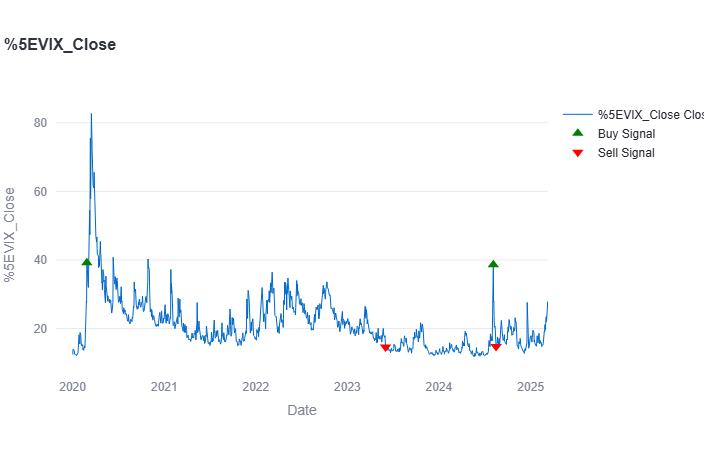

The strategies I’ve been testing use the CBOE Volatility Index (VIX) – often called the “fear gauge” of the market – to generate buy and sell signals for broad market ETFs like SPY (S&P 500) and QQQ (Nasdaq-100). The premise is straightforward: volatility patterns can help predict market direction.

The analysis is visible at https://rcsmit.streamlit.app/?choice=52 (‘wake up’ when necessary)

The code is at https://github.com/rcsmit/streamlit_scripts/blob/main/vix_bot.py

I analyzed three specific VIX-based approaches:

- The Omero Strategy: Buy SPY and QQQ when VIX exceeds 30 (high fear), sell when VIX drops below 15 (low fear)

- Moving Average Crossovers: Buy when the 50-day VIX moving average crosses above the 20-day moving average, sell when the 20-day crosses above the 50-day

- Bollinger Bands: Buy when VIX moves above the upper Bollinger Band, sell when it drops below the lower Bollinger Band

The Surprising Results

While these strategies have historical merit, my testing revealed something interesting: they only consistently outperform when starting from January 1, 2022 and using the Moving Average Crossovers and Bollinger band strategy. The Omero strategy is never outperforming the market.

This finding highlights a crucial lesson in algorithmic trading – strategies often demonstrate period-specific effectiveness rather than universal applicability. Let’s dive into why this might be happening.

Market Context Matters

The period beginning January 2022 was characterized by:

- The transition from an ultra-low interest rate environment to aggressive rate hikes

- Heightened inflation concerns after pandemic-era stimulus

- Geopolitical tensions with the Russia-Ukraine conflict

- Significant tech sector volatility and the beginning of a valuation reset

These conditions created precisely the type of volatility regime where VIX-based strategies tend to shine. The VIX experienced multiple significant spikes during this period, providing clear signals that the strategies could leverage.

The Key Insight: January 2022 Start Date Advantage

While examining these strategies, something crucial is visible: despite the buy and sell signals at various points, the portfolio value largely follows the overall market trajectory. The strategies only consistently outperform when starting from January 1, 2022.

This timing advantage occurs because starting in 2022 allows investors to avoid the significant market dip in late 2021, effectively skipping a period of underperformance. By avoiding this drawdown phase, the compound ROI calculation benefits substantially – you’re essentially measuring performance from a local bottom rather than including the preceding decline.

This insight highlights a fundamental truth in backtesting: your starting point can dramatically impact perceived performance, even when the underlying strategy remains identical.

Have you experimented with VIX-based trading strategies? I’d love to hear about your experiences in the comments below.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. Always conduct your own research and consider your financial situation before making investment decisions.